Britain’s plan for growth is dead for now.

Prime Minister Rishi Sunak’s government is focusing instead on filling a deep hole in the public finances caused by rising interest rates, rocketing inflation and a likely recession, all of which have exhausted the resources available for stimulating the economy, an official with knowledge of the matter said.

That conclusion indicates the scale of the job facing Sunak and his Chancellor of the Exchequer Jeremy Hunt as they draw up the Treasury’s autumn economic statement due on November 17. While Liz Truss emphasized growth as the primary ambition during her few weeks in office, Sunak and Hunt are having to firm up investor confidence by showing how they will pay off the UK’s burgeoning debt load.

It’s one of the brutal ironies of Truss’s tenure. Her “growth plan” offering £45 billion ($52 billion) of unfunded tax cuts so spooked investors and damaged the UK’s fiscal credibility that it has killed off any immediate hopes of delivering long-term measures to bolster economic performance that the UK so desperately needs.

“The immediate focus needs to be on landing the fiscal consolidation,” said Tim Pitt, a former Treasury adviser now partner at Flint Global. “A clear, considered growth plan is essential, but it might make more sense to that as part of a budget in the spring.”

On Friday, people familiar with the government’s thinking said the Treasury is looking for tax increases and spending cuts totaling as much as £50 billion. That would add to headwinds the economy faces at the same time consumers are suffering the tightest cost-of-living squeeze in decades and the Bank of England plans the fastest increases in borrowing costs in 33 years.

Jeremy Hunt, UK chancellor of the exchequer.

Early steps by Hunt to reverse Truss’s package have restored some calm to financial markets, bringing down interest rates in financial markets and potentially saving up to £15 billion a year in debt service costs from the peak of the market panic a few weeks ago.

But that still leaves £35 billion needed, a sizable sum for an economy that’s sputtering. It marks a consolidation of about 1.5% of gross domestic product, equivalent to roughly a sixth of the budget squeeze between 2010 and 2018, the years of austerity after the financial crisis. For now, growing the economy is now a second-order concern.

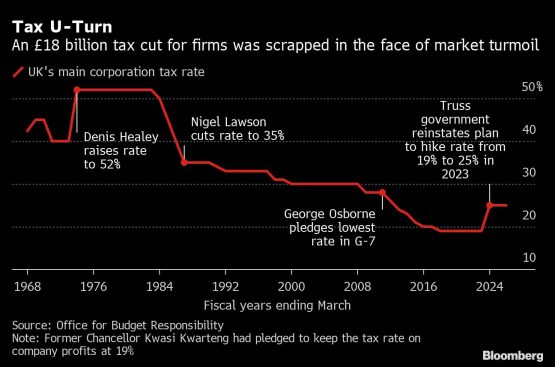

As chancellor in March, Sunak signaled that his flagship growth policy would be a major new tax relief to boost business investment. He can no longer afford it, according to one government official, who asked not to be named because budget discussions are still ongoing. That will mean the UK’s corporation tax rate rises to 25%, the most in a decade, from 19%, with little offsetting incentive for companies to invest.

Hunt is likely to promise deregulation, including financial-services reform, to drive longer-term output, but there will be no money for investment now nor will there be political backing for greater migration to address the UK’s chronic labor shortages. According to the Office for Budget Responsibility, lifting net immigration by 75 000 a year would raise long-term trend growth from 1.4% to 1.6%, still well below the levels prevailing in previous decades.

Sunak said “mistakes were made” under Truss, and as a result the government will now have to take “difficult decisions” on tax and spending to fill the remaining hole.

The Bank of England may be able to deliver a bit of help. The central bank on Thursday is expected by investors and economists to raise interest rates three-quarters of a percentage point to 3% and forecast a deeper recession due to “materially higher” rates than it projected in August, according to Nomura’s European economist George Buckley.

If its forecasts show inflation falling below target during the coming recession, investors may respond by lowering market rates. That would reduce debt-servicing costs and spare the government some austerity.

BOE officials already have signaled some softening in their hawkishness on rate rises. Deputy Governor Ben Broadbent earlier this month questioned whether “official interest rates have to rise by quite as much as currently priced in financial markets.” Extrapolating from the OBR’s rule-of-thumb calculations on the drop in market rates since then, his comments alone may save the Treasury £5 billion.

Even so, there will be no escaping hard decisions. Among the options on tax are:

- Expanding the windfall tax on North Sea oil and gas producers to all energy providers. Shell Plc’s chief executive conceded this week there was a case for windfall taxes as quarterly profits doubled to £8 billion. Could raise £5-£10 billion

- A bank tax to recover the profit lenders are making from the combination of higher interest rates and the stock of money created through quantitative easing. Could raise £2-£5 billion.

- Reintroducing the Health and Social Care Levy in 2024, which Sunak announced earlier this year and Truss scrapped. Potential: £15 billion.

- A flat rate of pensions tax relief of 25%. It would penalize higher-rate earners, who amassed savings during the pandemic and enjoy 40% relief, but encourage lower-rate earners on 20% relief to save. Could raise £5 billion.

- Increase capital-gains tax rates closer to levels charged for income. Could raise £3-£4 billion.

On spending, the options available include:

- Reducing public investment projects to past annual averages of 2% of GDP. According to the Institute for Fiscal Studies, that could save £14 billion.

- Freezing the foreign aid budget at 0.5% of GDP instead of boosting it as planned to 0.7% in 2024/25. Could save £5 billion.

- Benefits are under scrutiny despite the cost of living crisis and Hunt’s pledge to be “compassionate.” The government has not ruled out suspending the state pension triple lock. Uprating both the state pension and working-age benefits in line with earnings rather than prices would save £13 billion. Excluding pensions would still save around £7 billion.

Unprotected government departments — those outside health and education — are under pressure to find savings. But they are already having to cut between 8% and 10% of their budgets just to stick to existing spending limits.

The current limits on cash spending were set in 2021 before inflation and wages took off and drove up day-to-day costs. Making deeper cuts would risk a deterioration in public services already struggling after years of austerity.

Hunt may resort to accounting tricks. The government could decide to limit departmental spending increases after the current period ends in 2024 to 1% more than inflation. That would be below the convention of increasing budgets in line with GDP, and could save up to £10 billion.

Similarly, the four-year freeze on income-tax thresholds may be extended two more years beyond 2026. Doing so would save £2 billion annually, according to Resolution Foundation research director James Smith. Yet it would fly in the face of the government’s stated aim of lowering the UK’s long-term tax burden.

© 2022 Bloomberg