Introduction

It has been about three months since I last discussed Sun Life Financial (SLF) and I wanted to check up on this Canadian insurance company. I was interested to see if the company was able to boost its profitability after a weak first quarter.

Data by YCharts

Data by YChartsAs Sun Life’s average daily volume on its NYSE listing is almost 600,000 shares per day, there’s no specific need to trade in the company’s shares using the TSX listing. However, as Sun Life is reporting its financial results in Canadian dollars, I will use the CAD as base currency throughout this article while I also will refer to its Canadian listing (for consistency with the currency it’s reporting in).

Sun Life’s income statement turned positive again

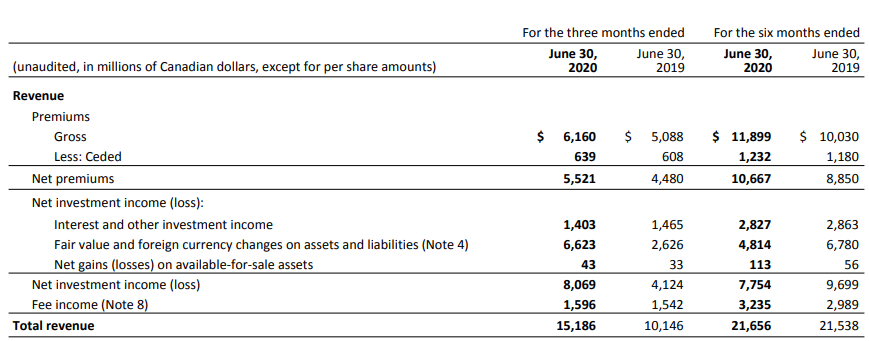

In the second quarter, Sun Life’s premium income increased again, both compared to Q1 2020 as well as compared to Q2 2019. And whereas the total revenue came in at C$10.15B in Q2 2019, the total revenue in Q2 2020 increased to C$15.2B thanks to a strong performance of the investment portfolio.

Source: Half-year report

That hardly is a surprise as the fair value decrease of approximately C$1.8B in the first quarter was an exceptional occasion and the fair value of assets increased again throughout the second quarter as the losses were reverted into a very strong fair value increase of C$6.6B.

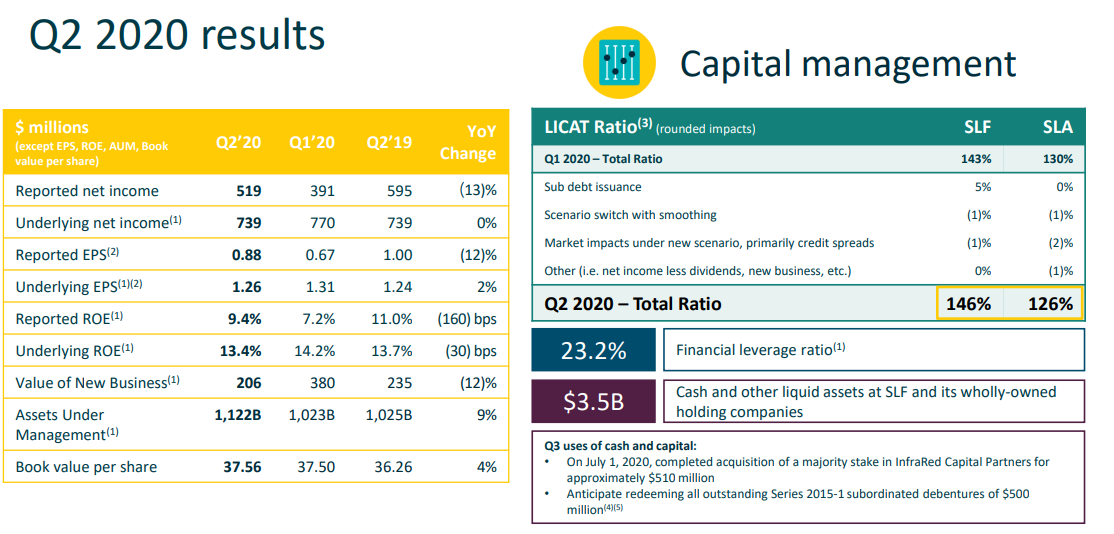

The total amount of benefits and expenses also increased and this resulted in a pre-tax income of C$713M and a net income of C$543M attributable to Sun Life (after deducting a C$105M net income attributable to the non-controlling shareholders). Of the C$543M, about C$24M was earmarked to cover the preferred dividends (which I discussed in depth in the previous article) leaving C$519M on the table in net income attributable to the common shareholders of Sun Life. This represented an EPS of approximately C$0.89 and still more than fully covers the C$0.55 quarterly dividend.

Source: company presentation

A closer look at the income generating assets on the balance sheet

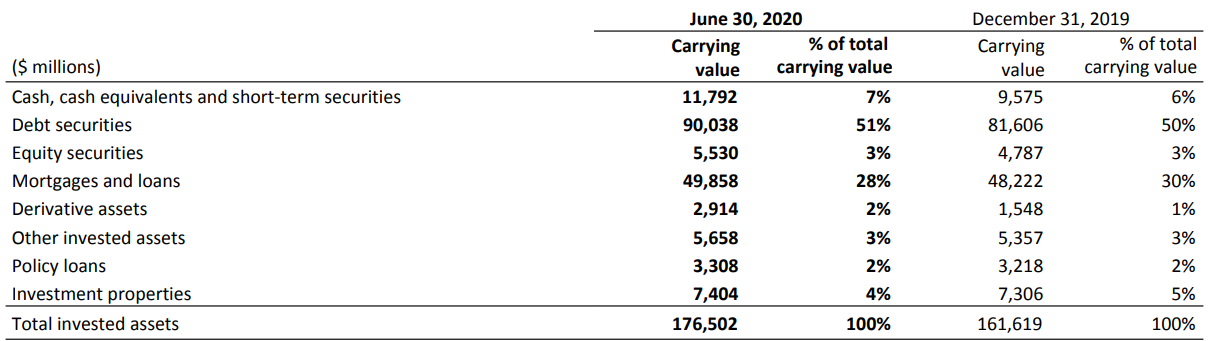

Looking at Sun Life’s balance sheet, we see the company has invested almost C$177B in assets that should hopefully generate a solid positive return. The assets are broken down as follows:

Source: Company half-year report

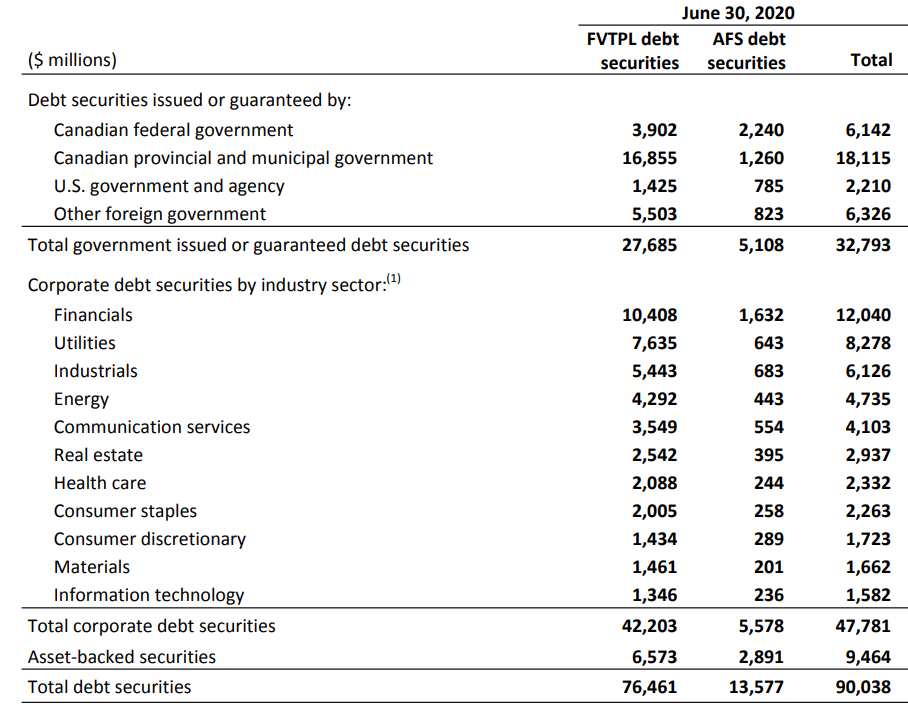

As the debt securities and mortgages make up the bulk of the invested assets (together with the cash position, in excess of 85% of the assets are in these three asset classes). Fortunately Sun Life provides a relatively decent breakdown of the investments in debt securities, and we see in excess of those debt securities are government issues:

Source: half-year report

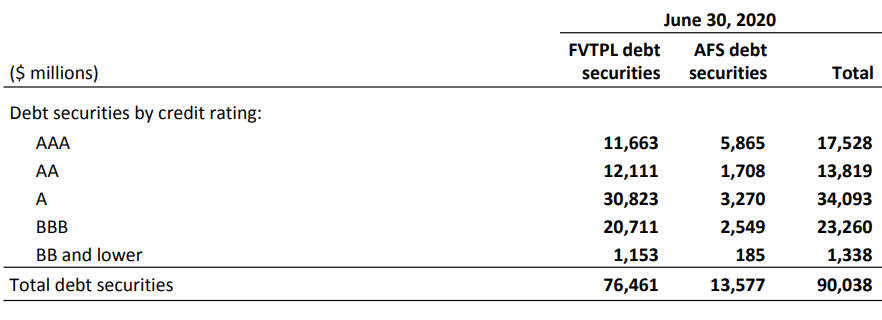

The remaining C$57B of debt securities consists of corporate debt (and some asset-backed securities). It looks like Sun Life is definitely still focusing on asset quality as in excess of 70% of those securities have a credit quality ratio of A or higher and less than 2% has a credit quality score of BB and lower, as you can see below:

Source: half- year report

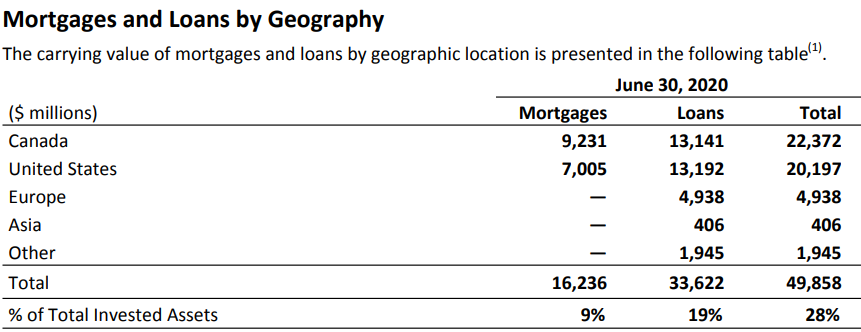

Sun Life also disclosed its exposure to the oil and gas sector for C$5.5B, the transportation sector for C$3.8B and the hotel sector for C$1.1B. What piqued my interest was the C$14.8B exposure to office, retail and residential property types in the commercial mortgage portfolio.

Source: half-year report

Fortunately the average LTV ratio of the mortgage portfolio is just 54%, so despite the exposure to office and retail properties, I’m not too worried about the quality of Sun Life’s mortgage book. Even if the real estate market completely collapses and a 40% haircut is warranted, Sun Life’s LTV ratio is low enough to absorb a huge blow like that. The loans divisions provides less visibility as of the C$33.6B in loans, just about 55% has a credit quality score of A or higher. 40% of the loan exposure has a credit quality score of BBB.

Investment thesis

Sun Life’s asset portfolio appears to be very well diversified and sure there are some assets that are barely investment grade, but as those assets make up a very small part of the investment portfolio, I’m not too worried. Sun Life saw the investment losses in Q1 revert in Q2 and remains a healthy company.

Unfortunately the dividend yield has now dropped to just more than 4% while most of the preferred shares have now also seen their yield decrease to less than 5% as the markets are now less nervous than a few months ago. In these situations I tend to prefer writing an out of the money put option and the P46 (which is approximately 15% lower than the current share price) expiring in January 2021 has an option premium of in excess of C$1. This would indicate that if these put options expire in the money, the dividend yield on the common shares would increase to almost 4.9%. Right now, I have no position in Sun Life (nor in its preferred shares) and an out of the money put option would probably be my preferred way to re-establish a position below the current share price.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

NEW at ESCI: A dedicated EUROPEAN REIT PORTFOLIO!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.